Revolutionising Personal Finance Management Apps

The Hook

Not another expense tracker. An AI finance buddy that actually helps.

Most PFM apps do one thing really well. They show you your own data. Nice charts, neat categories, monthly summaries. "You spent 12k on food" and all that.

But after the first few days, the feeling is always the same: "Okay, I can see it. Now what?"

That is the real reason PFM apps have high churn. Dashboards do not change behaviour. People do not open an app every day just to feel guilty looking at a pie chart.

That gap is exactly why we built MoneyPal.

The Problem

Traditional PFM apps stop at tracking

From observation, and honestly from personal experience, most PFM apps help you record expenses, show where money went, maybe set a budget limit. But they do not tell you what to fix, what matters first, or what to do next.

MoneyPal was designed around action, not just awareness.

The Solution

Five things that make MoneyPal different

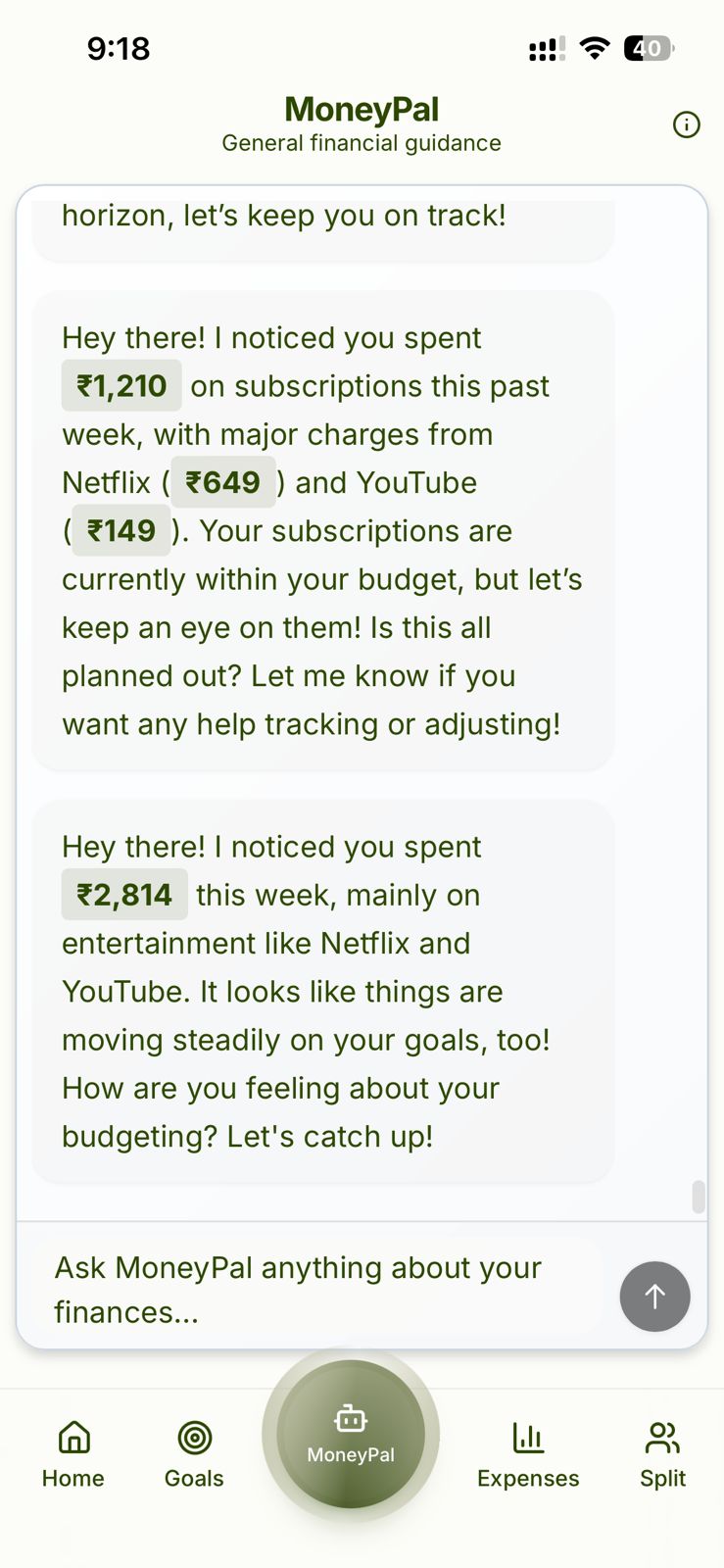

A proactive AI that gets involved in your day-to-day spending

Instead of waiting for the user to open the app, MoneyPal's AI is proactive. If you're overspending on Swiggy this month, the app doesn't just show it at month-end. It tells you in the moment, when it still matters.

We designed MoneyPal like a buddy that watches your budgets and nudges you when you're going off track. Not in a preachy way. More like: "Hey, you're close to crossing your food delivery budget. Want to slow down for the rest of the week?"

This is the difference between a tracker and a coach.

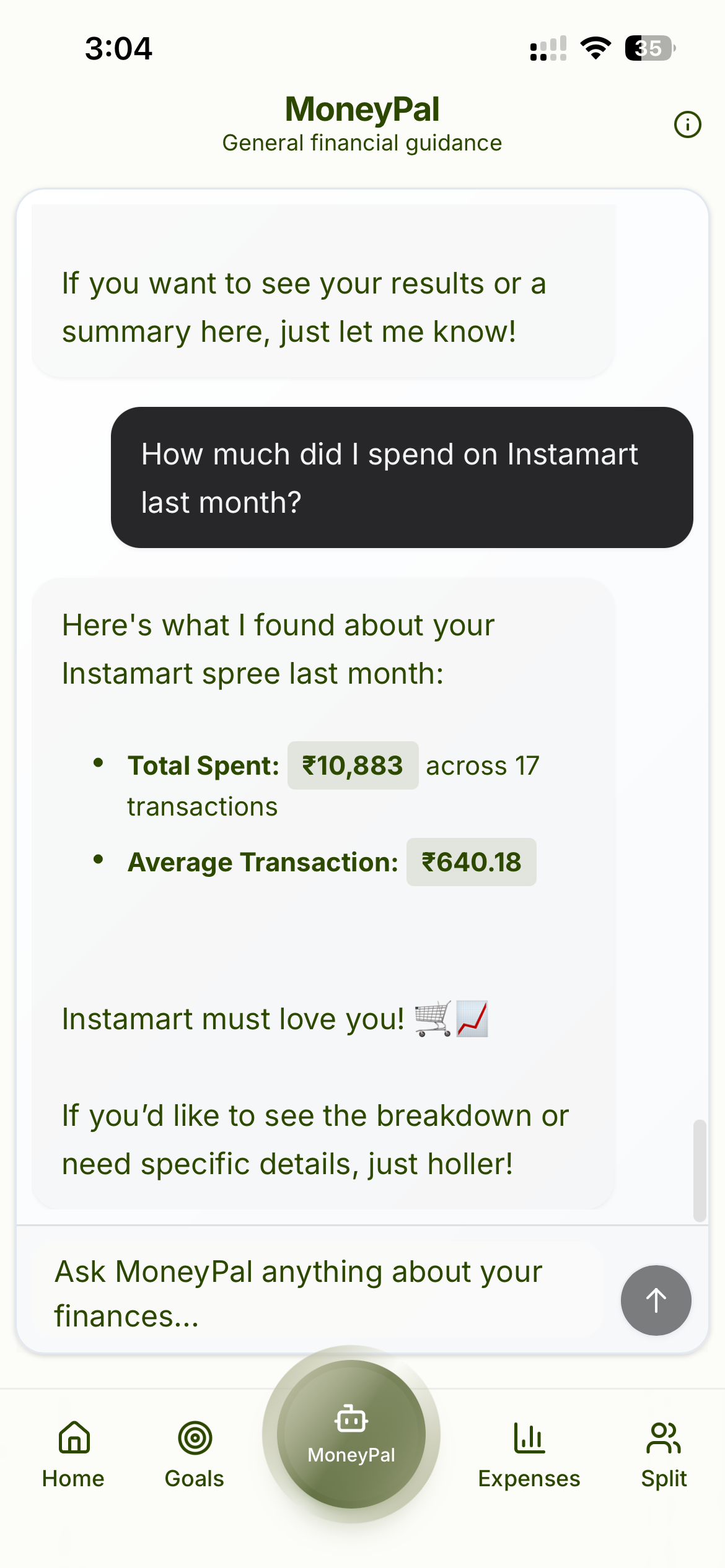

Ask anything. The AI answers in plain language.

A big frustration with finance apps is that even when the data is there, you still have to dig through filters, categories, and screens to find the answer. MoneyPal flips that.

You can ask things like:

• "How much did I spend on food delivery this month?"

• "Grocery spend last month vs this month?"

• "What are my biggest recurring expenses?"

• "How much am I saving after rent and bills?"

The AI answers directly, with numbers, context, and a short explanation. The goal is to reduce effort. If getting answers feels like work, users won't come back.

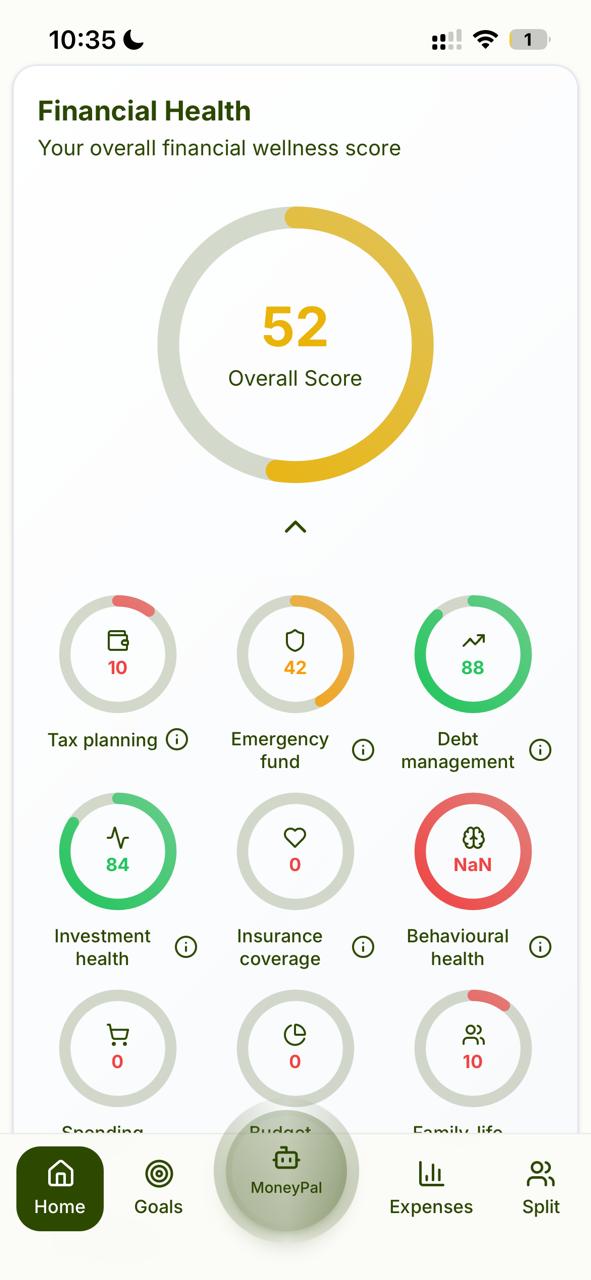

Financial Health Score: what you're lacking, not just what you spent

Most apps tell you spending categories. No app tells you: "Here are the financial areas where you're weak."

MoneyPal gives you a Financial Health Score broken into real-life buckets:

• Tax planning

• Emergency fund

• Debt management

• Investment health

• Insurance coverage

• Behavioural health (spending and budgeting patterns)

• Family and future planning

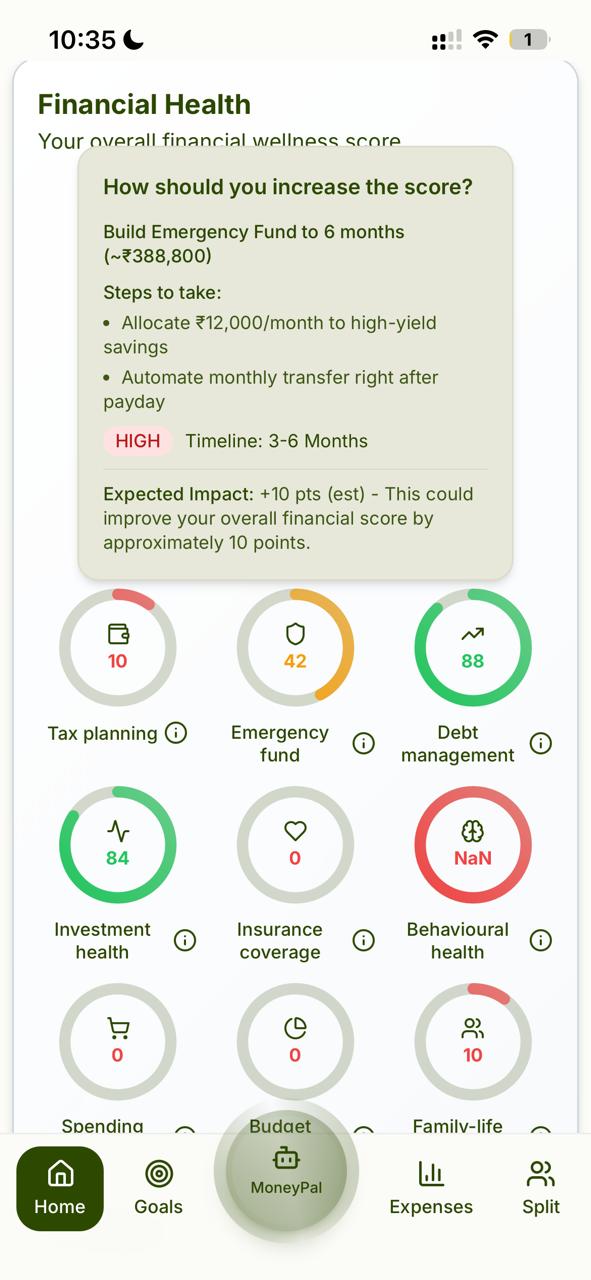

And it doesn't stop at scoring. It tells you what to do next. If your emergency fund is weak, MoneyPal suggests a clear target (6 months buffer), gives monthly saving steps, shows expected impact, and a timeline.

This turns finance into a game you can improve at, instead of a report card you avoid opening.

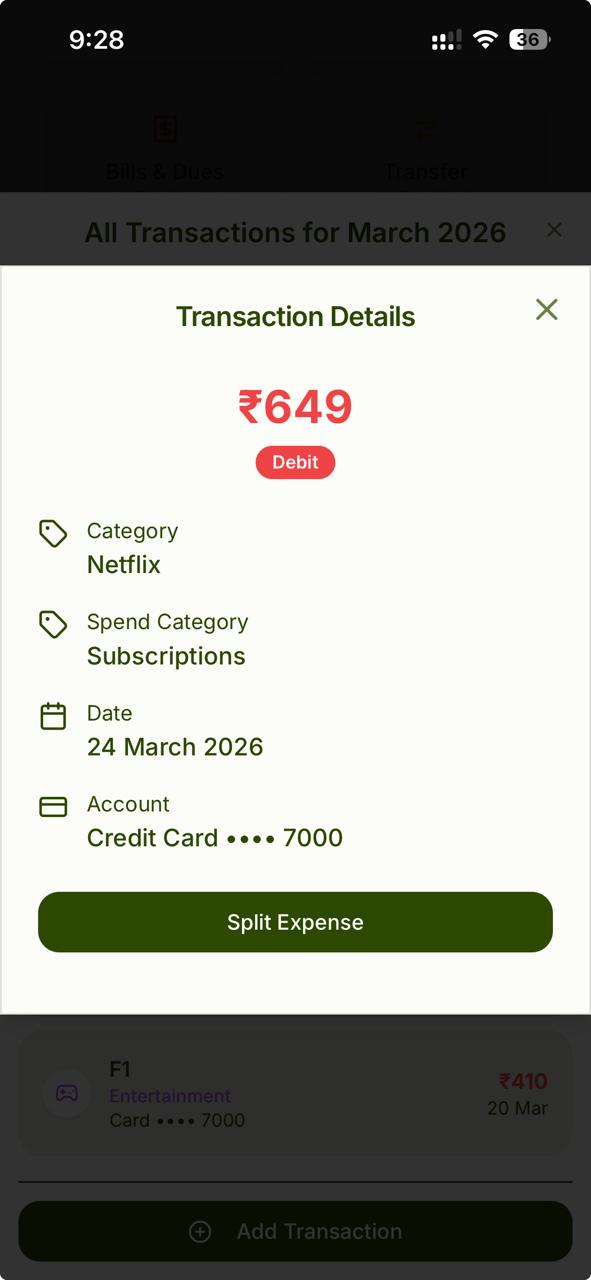

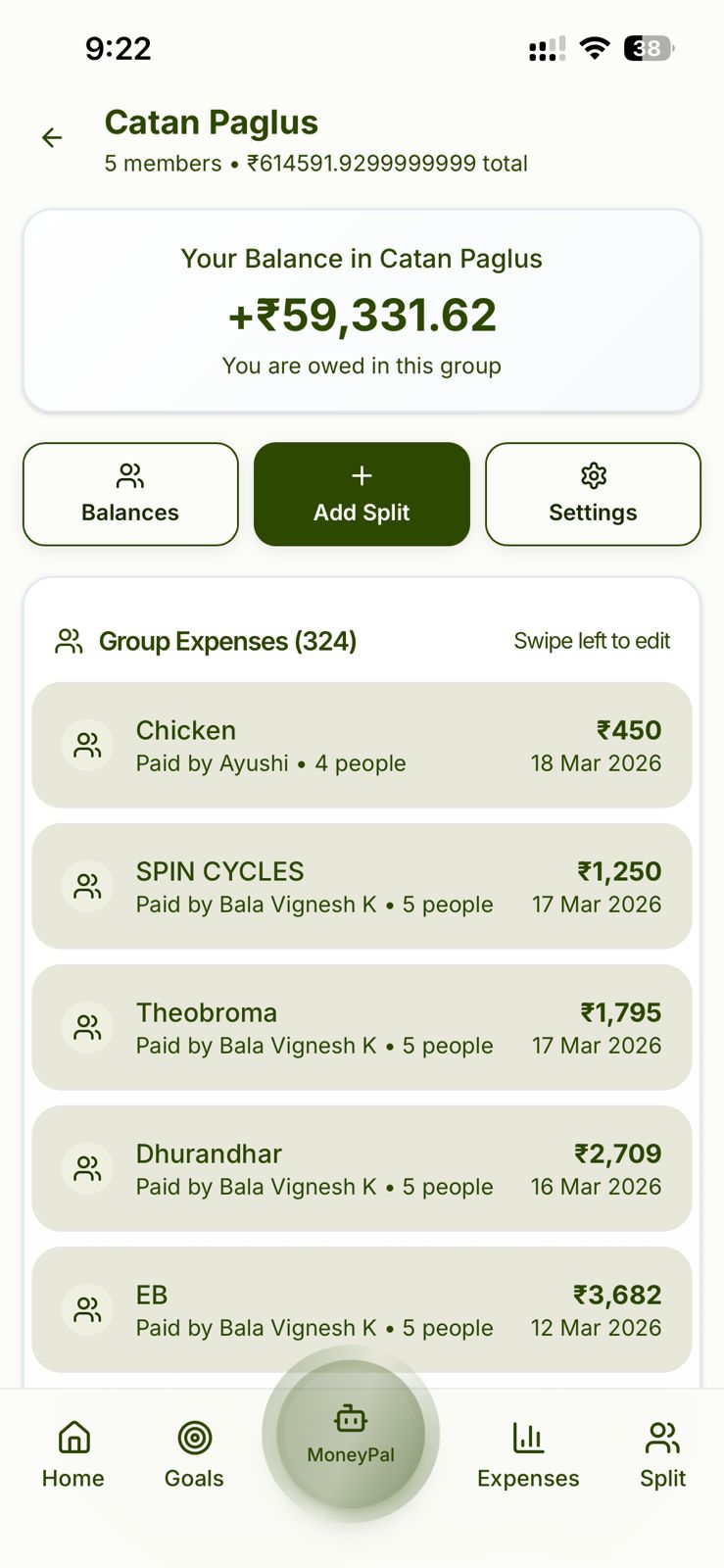

One-tap split for shared expenses, because manual entry is painful

Splitting expenses with existing apps means manually adding the expense, selecting people, entering amounts, and repeating. It works, but it feels like homework.

In MoneyPal, transactions are already being read. So splitting should be effortless.

The flow:

• Transactions are auto-read

• Select one

• One tap to split with your group or friend

Instead of "entry first, split later", it becomes "transaction first, split instantly". This makes splitting feel natural and fast, which is what people want in real life.

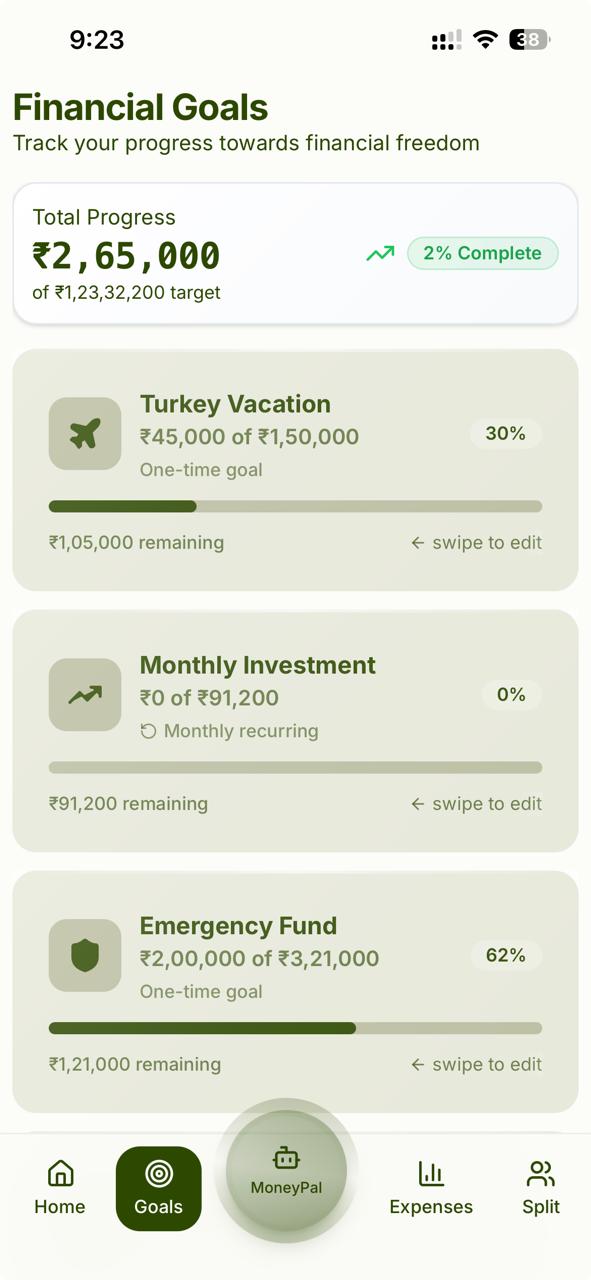

Goals and budgets: set with you, tracked for you, nudged when you deviate

Most people don't know what budget to set. Or they set something random and forget it in 3 days.

MoneyPal's AI helps users set goals and budgets based on what they want to achieve:

• "I want to save 20k a month"

• "I want a 3 lakh emergency fund"

• "I want to reduce food delivery spend by 30%"

Then the app tracks progress and nudges users when they're deviating.

Tracking alone is passive. Tracking plus nudges becomes behaviour change.

Why It Matters

MoneyPal is not trying to be another place where your financial data sits.

It is trying to become the layer between your spending and your decisions: a buddy that answers your questions without effort, shows where your financial foundation is weak, tells you what to fix first, keeps you accountable with nudges, and removes friction in everyday things like splitting expenses.

Answers your questions without effort

Shows where your financial foundation is weak

Tells you what to fix first

Keeps you accountable with nudges

Removes friction in everyday tasks like splitting

MoneyPal · 2025